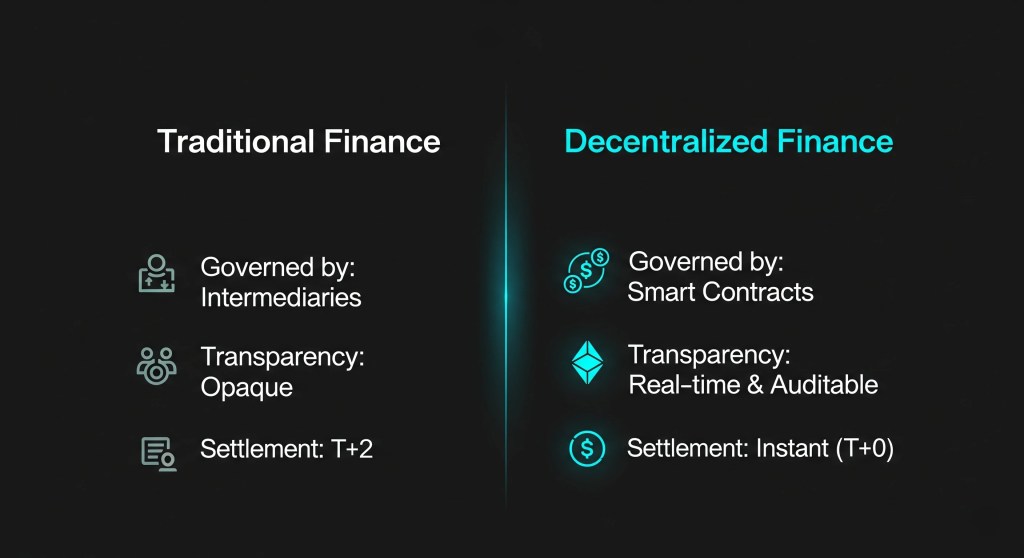

For the better part of a century, the fixed-income market has operated under a simple, universally accepted paradigm: a centralized architecture governed by central banks and intermediated by large financial institutions. This system, for all its power and scale, is defined by its inherent limitations: opacity, restricted access, and a reliance on intermediaries that introduce friction and cost. While this model built the modern financial world, a new ecosystem is emerging from the fringes of technology that presents a fundamental challenge to its dominance.

On the blockchain, a parallel fixed-income universe is taking shape. This world of decentralized finance (DeFi) protocols offers unprecedented transparency, global accessibility, and novel sources of yield, operating autonomously beyond the direct control of any single authority. This is not a niche experiment; with a total value locked (TVL) now exceeding $140 billion, it is a nascent financial system whose principles of transparency and efficiency are poised to redefine capital markets.

The New Machinery: Decentralized Lending Protocols

At the heart of decentralized fixed income are lending protocols—autonomous, code-based platforms that allow users to borrow and lend assets without an intermediary. Unlike a traditional bank, these protocols are governed by smart contracts on a blockchain, primarily Ethereum, which hosts nearly 60% of all DeFi activity.

The scale of this new market is already significant. As of August 2025, the lending protocol Aave stands as a titan in the space, with a TVL of $33.58 billion, commanding nearly 24% of the entire DeFi market. It, along with pioneers like MakerDAO ($6.5 billion TVL) and Compound, forms the core infrastructure for a new kind of credit market.

Instead of loan officers and credit committees, these protocols use algorithmic interest rate models. Rates are determined transparently by supply and demand, governed by a simple « utilization rate. » As the pool of available assets for borrowing shrinks, interest rates automatically rise sharply to incentivize new deposits. This creates a dynamic, self-regulating system that adjusts to market conditions in real-time, block by block.

Searching for Yield: DeFi vs. Traditional Bonds

The primary allure of this new ecosystem is its ability to generate yield in ways that traditional fixed income cannot. While a 10-year U.S. Treasury bond offered a respectable 4.34% in August 2025, and high-yield corporate bonds hovered between 7-9%, these returns are dwarfed by the opportunities in DeFi.

The new sources of yield are fundamentally different, driven by a combination of user fees, protocol incentives, and risk premiums:

Lending Yields

Supplying a stablecoin like USDT to a protocol like Aave has generated average yields of 5.6%, with peaks exceeding 15% during periods of high borrowing demand.

Staking Yields

Participants can earn rewards for securing blockchain networks. Staking Ethereum through a liquid staking protocol like Lido (the largest DeFi protocol with $37.7 billion TVL) currently generates a nominal yield of around 3.08%.

Yield Farming

This is the most aggressive strategy, where users provide liquidity to various protocols to earn a combination of trading fees and token incentives. While highly variable and risky, these strategies can offer returns of 10-30% or higher.

This yield premium is not a free lunch; it is direct compensation for the unique risks inherent in this nascent market.

The Promise of Radical Transparency

Perhaps the most revolutionary aspect of decentralized finance is its radical transparency. While traditional banks operate behind a veil of opacity, providing opaque financial statements on a quarterly basis, every transaction on a public blockchain is auditable by anyone in real-time.

A new generation of on-chain analytics platforms—such as Dune Analytics, Nansen, and DefiLlama—act as open-source intelligence agencies for this new financial system. With a simple query, an investor can monitor a lending protocol’s real-time health, track loan-to-value ratios, identify large whale movements that might signal risk, and verify the protocol’s reserves down to the last token. This stands in stark contrast to the traditional system, where a comprehensive understanding of a bank’s risk exposure is a privilege reserved for regulators.

A Balanced View: Navigating the Real Risks

The promise of this new world is tempered by significant and undeniable risks. The very code that enables these autonomous protocols is also their greatest vulnerability. The 2024-2025 period saw an unprecedented wave of security breaches, with total losses from hacks and exploits exceeding $3 billion.

- Smart Contract Security: Sophisticated attacks have become commonplace. The February 2025 hack of the Bybit exchange, attributed to North Korea’s Lazarus Group, resulted in $1.5 billion in losses due to compromised private keys. In May 2025, the Cetus Protocol was exploited for $223 million due to a single integer overflow flaw in its smart contract code. These incidents underscore the reality that in DeFi, code risk is investment risk.

- Regulatory Uncertainty: The second major risk is the evolving and fragmented regulatory landscape. While some jurisdictions are creating clear frameworks, major markets like the United States are still grappling with how to classify these new instruments and protocols, creating a persistent cloud of uncertainty for institutional investors.

Implications for the Future of Capital Markets

The rise of decentralized fixed income represents more than just a new asset class; it is a paradigm shift. It challenges the very necessity of traditional intermediaries. In a world where credit risk can be assessed algorithmically and capital can be allocated via autonomous protocols, the role of large banking institutions will be forced to evolve. The future may lie in a hybrid model, where traditional finance provides the regulated gateways and institutional on-ramps to this new, more transparent, and efficient decentralized core.

Conclusion & Outlook

Decentralized fixed income is still in its early, experimental, and highly volatile stage. The risks of catastrophic losses are real and should not be underestimated. However, the fundamental principles it champions—transparency, accessibility, and efficiency—are undeniably powerful. The ability to create a global, open, and programmable credit market, free from the constraints and opacities of the legacy system, is a vision of profound importance. While the road to mainstream adoption will be long and fraught with challenges, the seeds of a new financial architecture have been planted. The future of bonds may not be intermediated by central banks, but governed by open-source code.